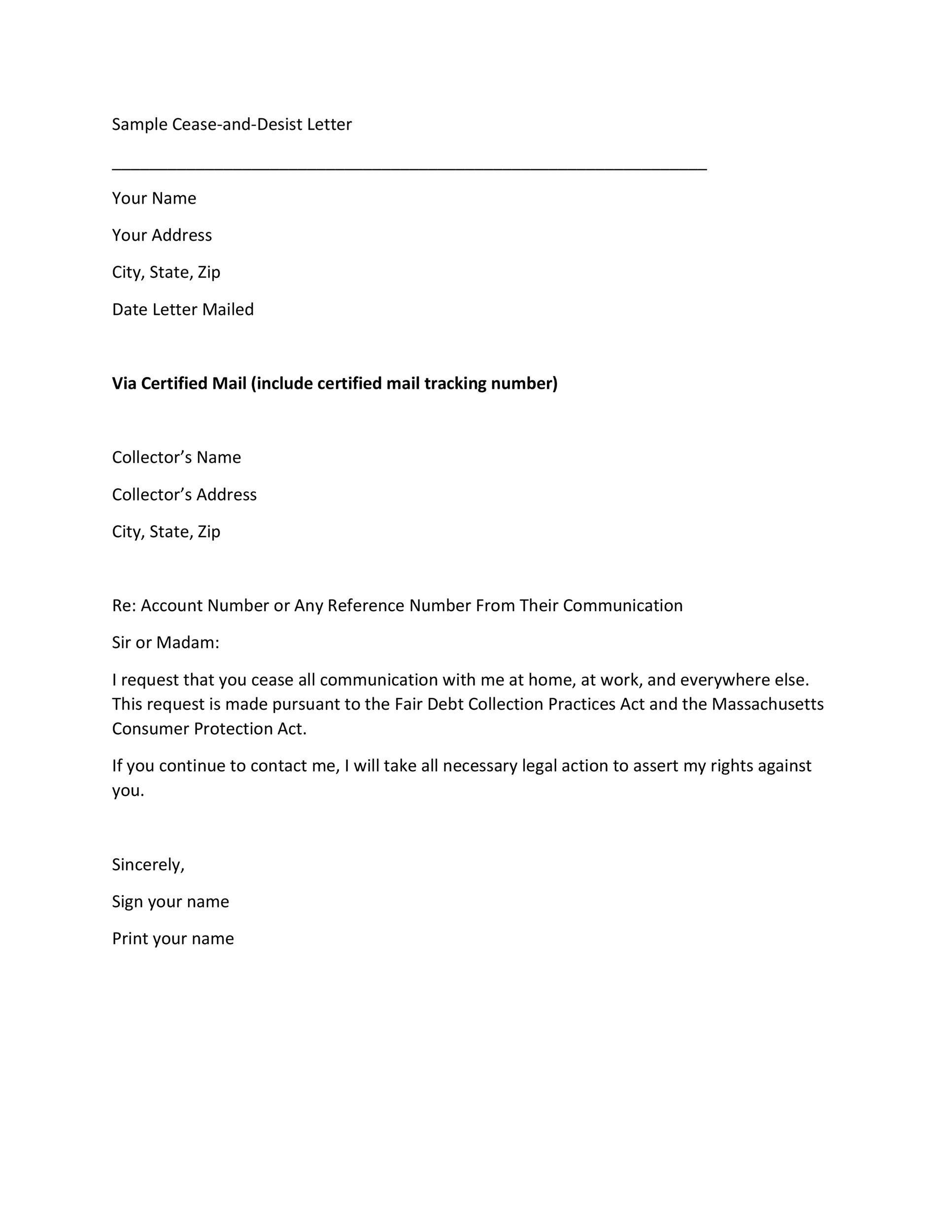

WhatsApp

WhatsAppPeople who want to handle big family home improvements or consolidate higher-desire financial obligation is utilize the home’s guarantee or take away a home collateral line of credit (HELOC). Instead of household security finance, which offer a lump sum payment, HELOCs is actually an effective revolving personal line of credit. You could borrow money as soon as you you need them-similar to a credit card. You may be considering an optimum borrowing count according to research by the security when you look at the your residence-generally as much as 85% of the house’s worth without one kept mortgage payments. If it pertains to you, listed here are five pros and cons to taking out fully a property collateral personal line of credit.

Virtually no closing costs

Settlement costs having HELOCs is lower than what it can cost you to intimate a mortgage, as the loan types having HELOCs is smaller than a standard home loan. Closing costs for HELOCs generally speaking work at anywhere between 2% in order to 5% of full credit line and add origination costs, underwriting fees, or other administration charges. Based on their lender, some of these prices are quicker otherwise got rid of. Such as for example, particular lenders get waive origination charges otherwise give no cash owed at the closing.

Your home is collateral

In the place of playing cards or personal loans, which happen to be unsecured, HELOCs try secure, meaning that a type of equity is required to borrow funds. Secured loans will often have lower interest levels but suppose specific risk. The fresh upside of your home being used as collateral would be the fact the greater amount of equity you’ve dependent, the greater number of you might be capable of borrowing from the bank. The fresh new downside of your home given that collateral is if you have overlooked a few mortgage costs, sadly, your property might be susceptible to foreclosures.

Your own home’s collateral are faster

As previously mentioned, HELOCs encompass borrowing from the bank from your own residence’s equity. When you build equity and certainly will acquire what you want, it is helpful. However, when the casing pricing decrease together with worth of your house falls, this may end in you due more than exactly what your house deserves. And you will, for individuals who owe more exacltly what the home is well worth, so it reduces your borrowing capabilities.

Adjustable interest levels

Rather than home collateral money, that provide fixed interest levels, HELOCs give varying interest levels. The rate fluctuates through the years-constantly subject to the newest Federal Set aside. Brand new Federal Set aside is responsible for form the fresh cost you to banking institutions fees one another to have right-away fund in order to satisfy set aside requirements. The prime rates is another benchmark speed and the most frequently made use of determinant regarding HELOC rates. The top rate is normally step three% greater than the new federal fund speed, and you will loan providers utilize this to put its rates. If Government Reserve transform new government money rates, other loan prices boost otherwise drop-off.

Likelihood of overspending

Regrettably, HELOCs aren’t notice-simply payments forever. From inside the draw months, you may be expected to create attract repayments. It may be simple to ignore how much you borrowed, especially when you’ve got a suck ages of a decade. In the event that draw period is over, you begin paying the principal level of your have a glimpse at this link loan, including attention. If you aren’t wanting or bookkeeping into upsurge in monthly money in case the draw period stops, it can been as an economic surprise.

Although it relates to tall idea, HELOCs can be a feasible choice if you have adequate equity made in your home using their freedom and potential taxation pros. However,, using your household because the security is going to be daunting for some. Test your financial patterns and view in the event that an effective HELOC works well with your situation. Please remember, Georgia’s Own is here to suit your credit requires, with aggressive ReadiEquity LOC costs .**

**Pricing is changeable and you may susceptible to changes. The Annual percentage rate (APR) may vary in the you to definitely shown and will also be according to your own credit history and you will financing in order to worthy of. Price might not surpass 18% at any time. Property and you may/or flood insurance coverage may be needed. Conditions, cost, and you can conditions try subject to alter without warning.

Recent Comments